Specialty Pharmacy Providers: Manufacturer Engagement and Contracting Trends

Highlights of the report:

Download a PDF of these Highlights

Specialty pharmacy providers' (SPP) regular and direct contact with patients make them uniquely positioned to be strong clinical & data partners that can enhance market access and shape the brand experience. HIRC’s report, Specialty Pharmacy Providers: Manufacturer Engagement and Contracting Trends, examines SPPs' evaluation of manufacturers and reviews contracting approaches with specialty pharmacies. The report addresses:

- Which pharmaceutical firms are most frequently nominated as SPPs' overall "Partner of Choice"? Which factors drive panelist selections?

- What types of clinical and data collaborations occur between manufacturers and specialty pharmacies to support brands? Which manufacturers most successfully engage SPPs in collaborative partnerships?

- Which manufacturers are most often nominated as having the best account managers and MSLs/HEORs calling on SPPs? What characteristics describe the best-in-class? H

- ow do 40+ manufacturers benchmark with SPPs in account management support and willingness to contract?

- How common are enhanced service and pricing/performance-based contracts between manufacturers and SPPs? How does this differ by therapeutic area and type of specialty pharmacy?

Key Finding: Pfizer, AbbVie, and AstraZeneca are among those best engaging specialty pharmacies in 2026; SPPs increasingly differentiate manufacturers based on collaboration quality, responsiveness, and account support rather than contracting alone.

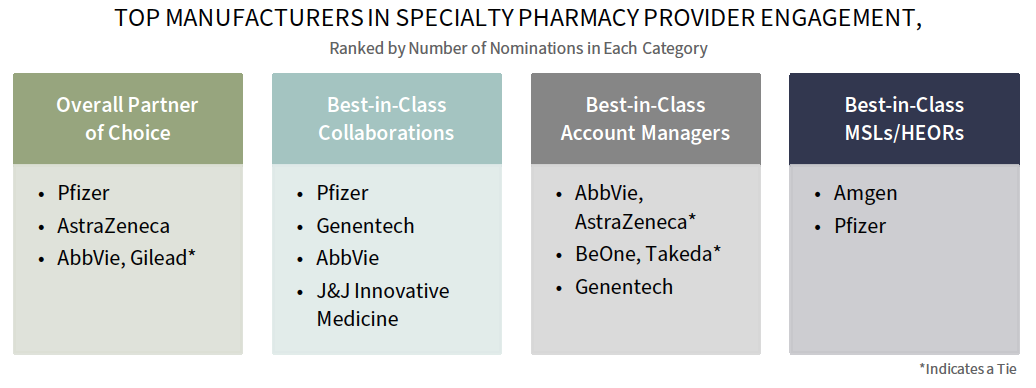

Pfizer Leads in Specialty Pharmacy Engagement in 2026. Specialty pharmacy provider executives were asked to consider and nominate a pharmaceutical manufacturer in four categories: (1) Overall Partner of Choice, (2) Best-in-Class Clinical and Data Collaboration Initiatives, (3) Best-in-Class Account Managers, and (3) Best-in-Class Medical/Clinical Science & Outcomes Liaisons. Pfizer consistently earns a top rank across categories, suggesting strong specialty pharmacy engagement to support its portfolio.

The complete report provides the full listing of all companies nominated as well as the factors driving nominations.

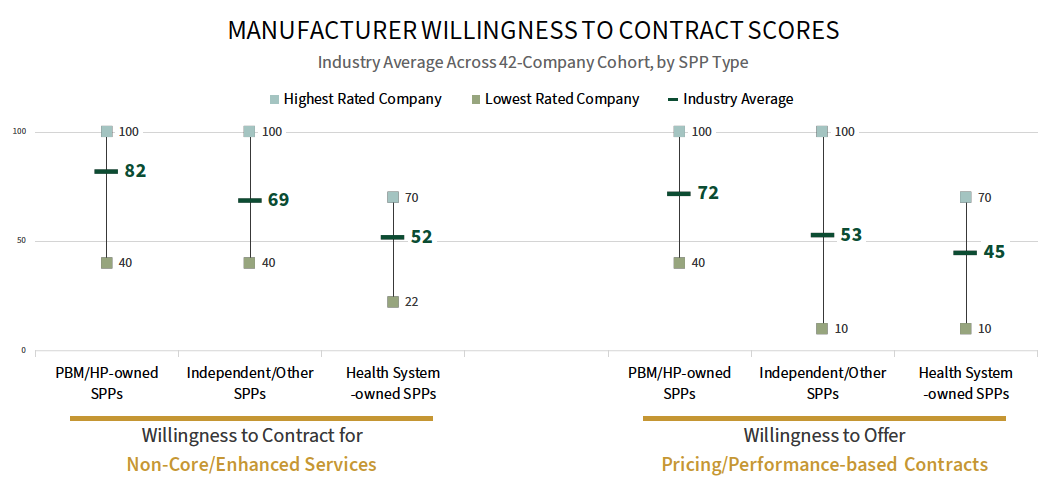

Approaches to Contracting with Specialty Pharmacies. Enhanced clinical and data service agreements, as well as pricing contracts, are increasingly viewed as important mechanisms for supporting specialty pharmacy sustainability amid growing reimbursement and margin pressure. Specialty pharmacy leaders were asked to rate a list of 40+ manufacturers in their willingness to engage in non-core/enhanced services contracting and pricing/performance-based contracting. Data suggest that manufacturers are more willing to engage in non-core/enhanced services contracting and that health system SPPs perceive a lower willingness to contract overall.

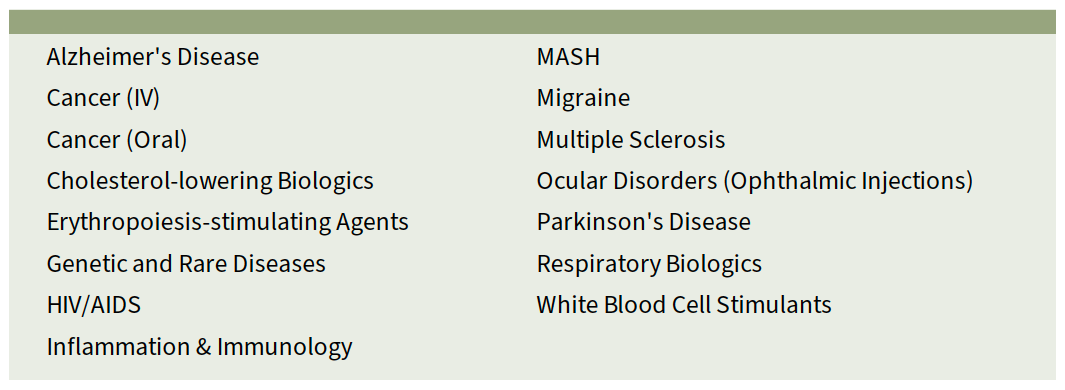

HIRC’s research also examines the prevalence of contracts across the following 15 high profile specialty therapeutic areas:

In addition to Willingness to Contract, HIRC benchmarks manufacturers in Presence with SPPs and Quality of Account Management Support. The full report examines analyzes all benchmarks and contracting data across three SPP ownership types: 1) PBM/Health Plan-owned SPPs, 2) Independent/Other SPPs (includes retail/drugstore chain, wholesalers), and 3) Health System-owned SPPs.

Research Methodology and Report Availability. In March and April, HIRC surveyed 46 specialty pharmacy provider executives, representing a variety of ownership types. Online surveys and follow-up telephone interviews were used to gather information. The report, Specialty Pharmacy Providers: Manufacturer Engagement and Contracting Trends, is part of the Specialty Pharmaceuticals Service, and is now available to subscribers at www.hirc.com.

Download a PDF of these Highlights

Download Full Report (Subscribers only) >